If you’re like me, and the oddsmakers, you thought the notion that Donald J. Trump would win the presidency was the definition of a long shot. And, if you’re like me — and 90% of the pundits, and 100% of the just-in-case put buyers — you thought the idea that, should the unlikely happen, the market would rally right out of the gate was the definition of the definition of a long shot.

And here we are breaking all-time highs by the day, with, as I continue to illustrate, a technical picture that says the bullish trend remains very much intact.

So, it has to be Trump, right? I mean, how else do you explain the market’s amazing performance since the election? Well, as I’ve preached herein ad nauseam, the factors that move markets are utterly uncountable and, therefore, impossible to know at any given time. The best we can do is assess probabilities based on the indicators we have at our disposal.

Let’s take another look. click any chart to enlarge

This chart shows the 50 and 200-day moving averages for the S&P 500 Index over the past 6 months:

That — the 50-day above the 200 and both sloping upward — is a very bullish setup. While pullbacks are inevitable regardless of the setup, the above screams buy the dips to the savvy trader.

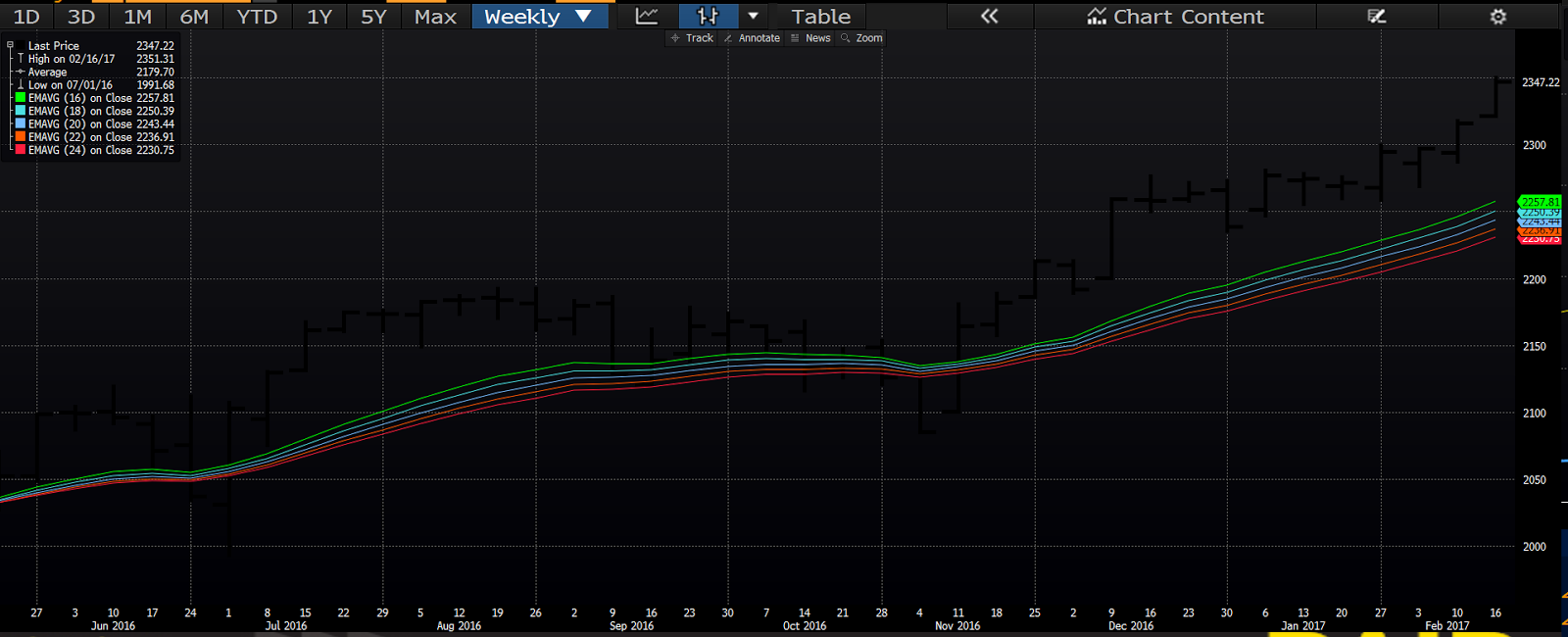

Now we’ll stretch it out a bit with a weekly chart and more sensitive exponential (assigns more weight to recent prices) moving averages:

That — the moving averages assembled perfectly (shortest [16-wk] to longest [24 wk]) — is a bullish setup as well.

So, we have a new president who promises to reform the tax code, deregulate businesses, repatriate corporate cash and spend a trillion bucks on bridges — and we have this positive setup — therefore, how can we not credit the man with the market’s recent gains? Well, again, there’s a lot at play when it comes to securities’ prices.

While I absolutely view the items I just mentioned as extremely (in the immediate-term) stock market-friendly, I see other stuff the president espouses to be extremely unfriendly to markets. I’ll simply fold the latter into the term protectionism.

Nobody articulates the lesson of history better than the late economist Hans Sennholz (emphasis mine):

In a world dependent on international trade and commerce, and staggering under a heavy load of international debt, no policy is more destructive than protectionism. It cuts off markets, eliminates trade, causes unemployment in the export industries all over the world, depresses the prices of export commodities, especially farm products of the United States. It is the crowning folly of government intervention.

If Sennholz, and yours truly, had/has it right — that protectionism is indeed a most destructive force — how is it that, amid all of the Administration’s protectionist threats, the market continues to mount all-time highs? Well, again, there’s also the promise of some hugely market-friendly stuff, so perhaps the good will simply overcome the bad. Or, perhaps Sennholz was, and I am, just plain wrong about what history, and, forgive me, commonsense says about protectionism. Or, given that market forces are too numerous to count, let alone assemble, perhaps it’s stuff not on our radar.

Or perhaps Jesse Livermore had it right:

Not even a world war can keep the stock market from being a bull market when conditions are bullish, or a bear market when conditions are bearish. And all a man needs to know to make money is to appraise conditions.

Hmm… You know, come to think of it, the “conditions” weren’t all that bad heading into the second half of last year. In fact, they were quite good:

The 50 and 200-day moving averages moved into bullish mode last April, and by mid-August they had virtually the same look they do today. And that was 3 months prior to the election.

And here are the weekly EMAs:

Yep, the exact same setup we have today.

Let’s add the index itself:

As you can see, the market — after a miserable start to the year — was doing well at a time when the notion of a Trump presidency was far-fetched indeed. So, no, with the setup as it was leading into the election, we simply can’t legitimately assign Trump all of the credit for the market’s recent run.

If you’re at all disappointed by my suggestion herein (if you indeed found satisfaction in the idea that the market rally is all about our new president), believe me, you shouldn’t be. In fact, anything that dispels the notion that the near or long-term success of your portfolio should hinge on the policies proffered by a single politician (talk about sitting on pins and needles!) ought to be music to your ears, and calming to your nerves.

Have a great weekend!

Marty