The Fed and The Bank of Japan are

holding their respective policy meetings today. I see a Fed rate hike as being highly

improbable, given that recent data – while on balance okay – doesn’t seem to be

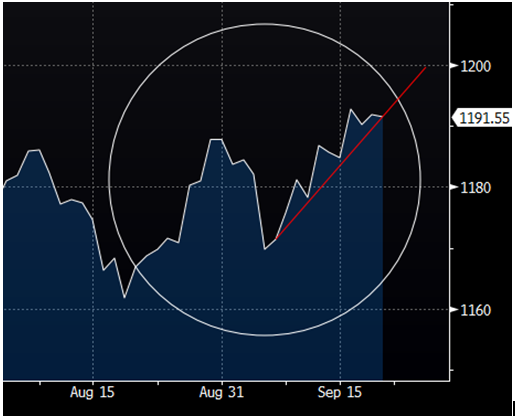

threatening enough relative to the signals the voting members have been sending. Plus, the dollar’s been rallying lately (first chart) and the Fed is clearly concerned

about bringing back the strong currency scenario that some would say has

tempered the recovery over the past couple of years: click charts to enlarge

holding their respective policy meetings today. I see a Fed rate hike as being highly

improbable, given that recent data – while on balance okay – doesn’t seem to be

threatening enough relative to the signals the voting members have been sending. Plus, the dollar’s been rallying lately (first chart) and the Fed is clearly concerned

about bringing back the strong currency scenario that some would say has

tempered the recovery over the past couple of years: click charts to enlarge

Therefore, assuming they don’t hike,

it’ll be all about the post-meeting commentary. Given the recent hawkish tone among an

increasing number of voting members, I suspect that the announcement and Janet Yellen’s press conference may yield a sterner warning to

the market that a hike is on the near-term horizon. If so, we may see the

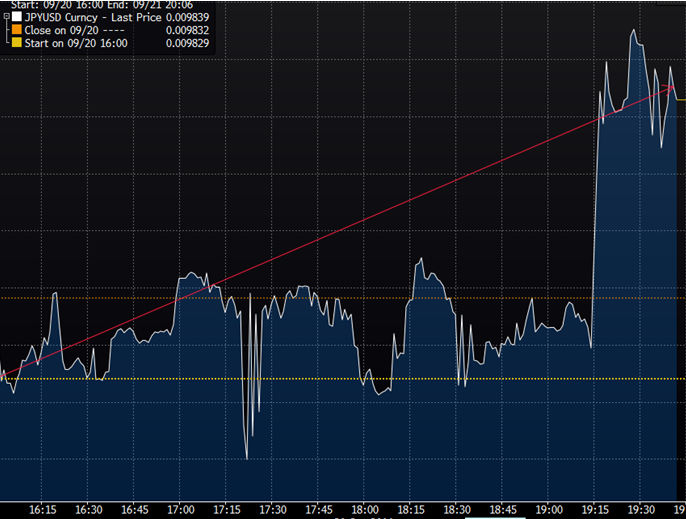

dollar rally anyway. It was actually up during equity market trading today:

Although it’s trading a little

lower as I type:

lower as I type:

Of course other forces will push

the dollar around as well. The Bank of Japan for instance has resorted to very

aggressive measures to devalue the yen (and, as a consequence, boost the dollar

[relative to the yen]), but to little avail. I had expected the BOJ to take yet

further measures of late, however, I believe that as the Fed rhetoric has

become more hawkish, Kuroda (BOJ’s head) is hoping that the U.S. Central Bank

will do the job for him. I.e., were the fed to hike, amid such an aggressive

Japanese monetary policy,surely presumably that would do a number on the yen.

the dollar around as well. The Bank of Japan for instance has resorted to very

aggressive measures to devalue the yen (and, as a consequence, boost the dollar

[relative to the yen]), but to little avail. I had expected the BOJ to take yet

further measures of late, however, I believe that as the Fed rhetoric has

become more hawkish, Kuroda (BOJ’s head) is hoping that the U.S. Central Bank

will do the job for him. I.e., were the fed to hike, amid such an aggressive

Japanese monetary policy,

The yen/dollar cross was all over

the map during the U.S. equity trading session today:

the map during the U.S. equity trading session today:

Trading higher since the close:

Clearly, currency traders are

expecting the BOJ to hold pat. If correct, that means the central bank is content

to risk somewhat of a Japanese equity market selloff if the Fed doesn’t deliver

on a rate hike tomorrow (again, unlikely) or on more aggressive language

(likely). It’ll then be keenly focused on the Fed’s December meeting. If the

Fed softens its language between now and then, I look for the BOJ to go deeper

into uncharted monetary easing territory.

expecting the BOJ to hold pat. If correct, that means the central bank is content

to risk somewhat of a Japanese equity market selloff if the Fed doesn’t deliver

on a rate hike tomorrow (again, unlikely) or on more aggressive language

(likely). It’ll then be keenly focused on the Fed’s December meeting. If the

Fed softens its language between now and then, I look for the BOJ to go deeper

into uncharted monetary easing territory.

One other central bank on the

docket this week is the Reserve Bank of New Zealand. They have a quandary of

their own — which is virtually the same as Japan’s. The New Zealand dollar has

been on a tear of late despite ongoing rate cuts:

docket this week is the Reserve Bank of New Zealand. They have a quandary of

their own — which is virtually the same as Japan’s. The New Zealand dollar has

been on a tear of late despite ongoing rate cuts:

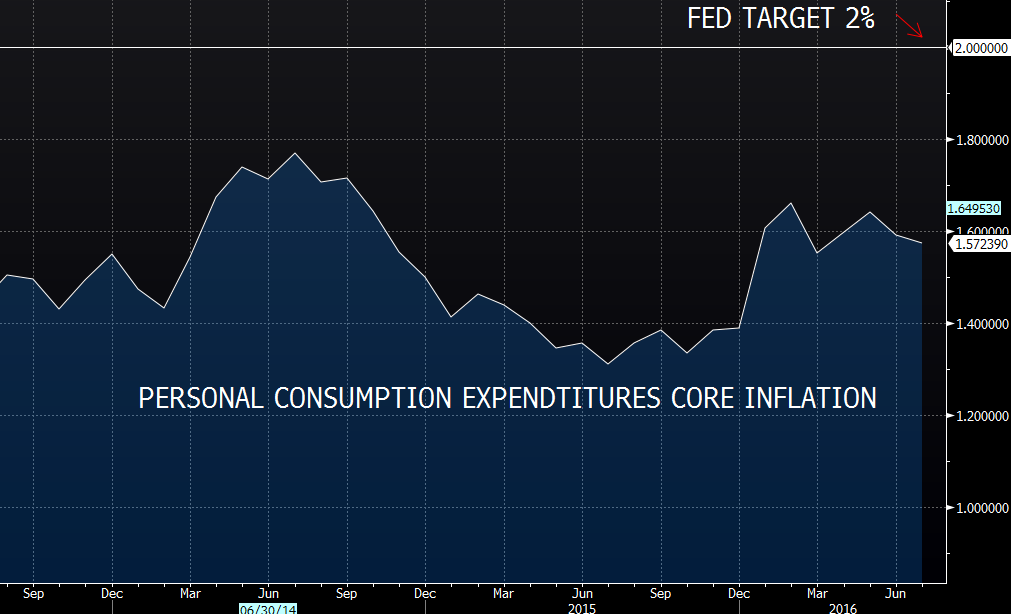

Fold in the easy monetary stance

of virtually the rest of the world’s central banks, and you have a higher U.S.

dollar risk that I don’t suspect the Fed is ready to exacerbate at this

juncture, particularly while U.S. (PCE) inflation remains below the Fed’s target.

of virtually the rest of the world’s central banks, and you have a higher U.S.

dollar risk that I don’t suspect the Fed is ready to exacerbate at this

juncture, particularly while U.S. (PCE) inflation remains below the Fed’s target.

All that said, their recent

rumblings smack of impatience. Could very well happen in December.

rumblings smack of impatience. Could very well happen in December.

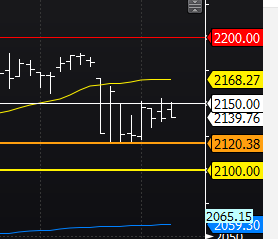

As for the stock market this

week, it’s been early morning rallies that get sold as the day progresses. The near-term

range for the S&P has been tight between 2150 and 2120. I think – if we get

a near-term upside breakout – it’ll see stiff resistance at 2200. If it breaks

lower, 2100 could be fairly strong

support.

week, it’s been early morning rallies that get sold as the day progresses. The near-term

range for the S&P has been tight between 2150 and 2120. I think – if we get

a near-term upside breakout – it’ll see stiff resistance at 2200. If it breaks

lower, 2100 could be fairly strong

support.

Of course anything can happen one day to the next. Which is perfectly okay for the prudent, patient, long-term investor! 🙂